Comments Off on Cryptocurrency Taxes Overview – How to Report Your Gains and Losses

An Overview of Crypto Taxes

Death and taxes are said to be the only things you cannot escape in life. When the latter is mixed with the world of cryptocurrency trading and investing, things can quickly become confusing and unclear.

In this article, we break down the fundamentals of cryptocurrency taxes for our traders that reside in the U.S. We discuss how the asset class is treated from a tax perspective and also outline the process for properly reporting the gains, losses, and income associated with your crypto trading activity.

Cryptocurrencies are Treated as Property

Contrary to what their name suggests, cryptocurrencies are not currently treated as currency in the eyes of some governments. The IRS (the tax collecting agency of the U.S) makes clear in its official virtual currency tax guidance that cryptocurrencies are to be treated as property for tax purposes.

What does this mean?

This means that all cryptocurrencies such as Bitcoin, Ether, XRP, and other altcoins need to be treated similarly to any other form of property like stocks, real-estate, or bonds from a tax reporting perspective.

In other words, capital gains and losses tax reporting rules apply to cryptocurrencies just like they do for stocks and bonds.

Cryptocurrency Capital Gains

Whenever you dispose of a cryptocurrency (get rid of it), you realize a capital gain or capital loss on the disposal.

The IRS considers all of the following to be disposal events for cryptocurrency (also known as taxable events):

Selling crypto for fiat

Trading one crypto for another

Using crypto to buy goods or services

Let’s take a look at a couple of examples to further illustrate how this works.

Example 1

Craig purchased 1 Bitcoin for $10,000 in April. Five months later, Craig sold that Bitcoin for $12,000.

In this example, Craig realizes a taxable event when he disposes of his Bitcoin by selling it for fiat. He realizes a $2,000 capital gain upon disposal (Sale Price – Purchase Price). Depending on what personal income tax bracket Craig falls under, he will pay a percentage of tax on this capital gain.

Example 2

John also purchased 1 Bitcoin for $10,000. However two months later, John traded 0.5 of that Bitcoin for 30 Ether. At the time, the 30 Ether was valued at $6,000.

In this example, John is disposing of his Bitcoin by trading it for ETH. This incurs a taxable event, and John realizes a capital gain or capital loss.

John’s cost basis for the 0.5 Bitcoin that he traded was $5,000 (0.5*10,000). The 30 ETH John traded for was worth $6,000 at the time of the trade, so John incurs a $1,000 capital gain on the transaction (6,000 – 5,000).

As you might have realized from these examples, calculating gains and losses can become quite tedious for high volume cryptocurrency traders—especially when you are actively trading crypto with on our automated trading products. This challenge stems from the fact that your crypto trades are most often quoted in other cryptocurrencies while your capital gains and losses need to be reported in your home fiat currency (US Dollar).

To effectively calculate your gain or loss from each trade, you need to know what the fair market value was in US Dollar for your cryptocurrencies at the time of the trade.

Data aggregators like CoinMarketCap can be used to track down this data by hand. Alternatively, cryptocurrency tax software products like CoinLedger.io can automate the entire crypto tax reporting and calculation process.

Do Capital Losses Reduce Your Tax Liability?

Yes! While capital gains increase your taxable income, capital losses lower it—meaning you’ll pay less to Uncle Sam by filing your losses.

In the U.S., you need to report each taxable event whether it is a capital gain or a capital loss. One common misnomer amongst traders is that if they lost money overall, they do not need to report. This is not true, and they will actually miss out on large tax savings by not reporting losses!

How Do I Report My Gains and Losses?

Capital gains and losses get reported on Form 8949. Simply report each taxable event (disposal) that you have within the tax year on a separate line of 8949. Once all disposals are entered, add them up to arrive at your net capital gain or loss.

For each row on 8949 you will need to include:

A description of the property sold

Original purchase date

Date sold

Proceeds from the sale (in USD)

Cost basis in the property (in USD)

Gain / Loss

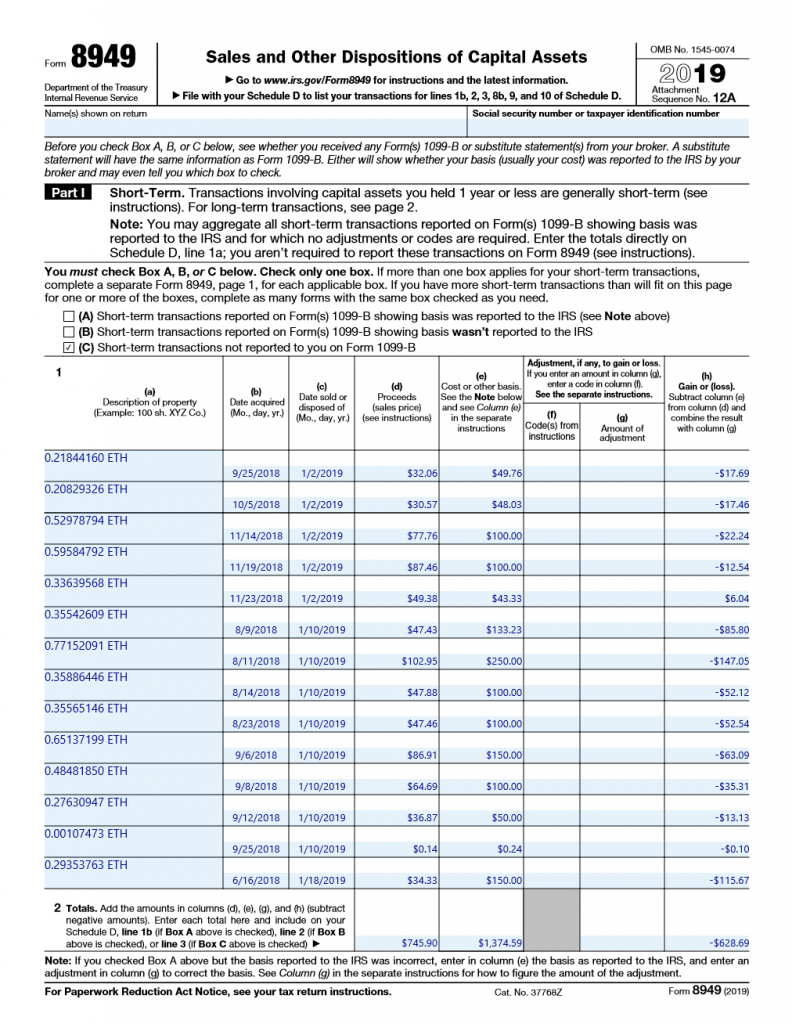

Below is an example of a filled out 8949 from a trader who was disposing of Ether.

IRS form 8949 with ETH example

Schedule D

Once you have your net capital gain or loss from all of your cryptocurrency disposals reported on 8949, you simply transfer this number to Schedule D of your tax return. Include both of these documents with your holistic tax return.

Cryptocurrency Tax Software

If you are looking for an easy way to automate your crypto tax reporting, it may be helpful to checkout some of the tools that have been specifically developed to help crypto traders with their tax reporting.

HaasOnline has teamed up with CoinLedger.io to help enable a more streamlined tax reporting for our U.S. traders.

CoinLedger integrates with most of the major exchanges we support to allow you to import your historical crypto transactions directly into their app. You can then generate your capital gains and losses tax forms based on this data with the click of a button.

HaasOnline users can use the discount code CRYPTOTAX10 to receive 10% off any CoinLedger.io report.

Tips & Tricks

To ensure that you will be able to easily report your crypto taxes at year end, make sure you are keeping track of the various exchanges and platforms you are using to trade. If you are a heavy user of multiple exchanges, it can be easy to lose track of everything you did over the course of the year. To avoid this, make sure to keep clean records.

Once year end comes around, you will easily be able to account for all of your trades and transactions with these records and get your tax reporting done in no time.

Comments Off on All About Cryptocurrency Taxes in 2023

Crypto Trading & Cryptocurrency Taxes

Trading cryptocurrency has become easier than ever, thanks to the development of sophisticated exchange platforms and new, user-friendly storage options. Yet there is one issue that can prove challenging for even relatively advanced traders: Cryptocurrency and taxes.

Given that the penalties for failing to accurately track, file, and pay taxes on cryptocurrency gains can be substantial, it’s vitally important that traders are equipped with up-to-date tax information.

With that in mind, let’s take a closer look at what you need to know about how to report cryptocurrency on taxes. You can also reference our other article about calculating crypto profit.

Do You Have to Pay Taxes on Cryptocurrency?

This is one of the most common questions among digital currency traders. If you’re in the United States, the short and simple answer is “yes” — cryptocurrency gains and losses must be reported on your taxes. Determining how to pay taxes on cryptocurrency — and how much you owe — is not so simple, however.

In the eyes of U.S. tax authorities, Bitcoin and other digital assets are not considered currencies, but rather property. Like stocks or real estate, cryptocurrency is a taxable asset that must be accounted for at the end of the year. Digital currencies are treated this way, in part, because they are typically used as investment vehicles, rather than a medium of exchange.

This has significant implications for those who buy and sell cryptocurrency. Unless you purchase your coins and tokens with the intention of holding them long-term, you need to be aware of the tax rules that govern any sale or trade of cryptocurrency. If you make any profit or sustain any loss from the sale of a digital asset, it has tax implications.

Cryptocurrency and Capital Gains Taxes

Because Bitcoin and other digital assets are treated as property by the IRS, they are classified as capital assets. This means that they are subject to U.S. capital gains taxes.

There are two forms of capital gains tax: Short-term and long-term. Short-term capital gains tax applies when an asset is held for 12 months or fewer. This is taxed at the same rate as your regular income. So, for example, if your income tax rate this year were 25-percent, any sale of a digital currency that you’ve held for less than a year would be taxed at 25-percent.

Long-term capital gains tax applies for assets held longer than 12 months, and the rate is variable. In 2018, long-term capital gains are taxed at zero-percent, 15-percent or 20-percent, depending on your taxable income and filing status. In many cases, investors will pay less in taxes by using long-term capital gains.

For example, a day trader who makes hundreds or thousands of Bitcoin trades each year — and who has a 30-percent income tax rate — would lose nearly one-third of any profits accumulated during the year to short-term capital gains tax. Someone who buys Bitcoin and holds it for a year could theoretically pay nothing in capital gains tax, assuming they earn less than $38,600 per year in regular income — the 2018 threshold for the zero-percent long-term capital gains bracket.

Another easy way to generate capital gains tax liability for your crypto trades in by using a service like CoinLedger.io.

Reporting Cryptocurrency on Taxes

Let’s take a closer look at the scenarios under which cryptocurrency taxes would need to be paid. First, the act of trading digital currencies would qualify. Any profit or loss on a trade is a taxable event. Additionally, selling cryptocurrency for cash (whether over the counter or to a friend) also triggers a taxable event, assuming there is a profit or loss.

If you accept cryptocurrency in exchange for goods or services — and that cryptocurrency goes up or down in value — that registers as a taxable event. The same thing applies to selling cryptocurrency to purchase items.

There are, however, some methods one can employ to reduce the tax burden associated with trading digital currencies. Margin trading, for example, allows you to maintain your core assets while deferring the capital gains taxes that would be triggered by a sale. This allows traders the flexibility to exploit developing market opportunities, without having to worry about steep, short-term capital gains taxes.

If you’re a crypto trader, you should also be aware that the IRS allows you to reduce your taxable income by deducting your losses. There is, however, a $3,000 maximum to this income reduction as of 2018. If you day trade for a living, you may also be able to deduct your trading expenses (establishing and claiming a home office for your business, for example).

How Cryptocurrency Taxes Have Evolved

Because Bitcoin was the first functional digital currency there was no real precedent for how cryptocurrencies would be treated under tax laws.

In the immediate aftermath of Bitcoin’s creation, there was little guidance on tax regulation, given Bitcoin’s newness, its obscurity and its lack of value. Bitcoins were initially trading for a few pennies, mostly among cryptography and computer hobbyists.

Once the popularity and value of Bitcoin began to soar, the regulatory landscape began to take shape. In 2013, Germany declared Bitcoin a unit of account and deemed it subject to capital gains tax. The following year the IRS issued Notice 2014-21, which provided guidance on tax issues surrounding virtual currencies and established that cryptocurrencies in the U.S. were subject to capital gains taxes.

In 2019 there was an update to U.S. Tax Codes

In October 2019, the United State’s Internal Revenue Service (“IRS”) provided official guidance on cryptocurrency taxation, which states that cryptocurrencies, including Bitcoin, Etherium, Litecoin, XRP, and so on should be treated as property for tax purposes, as opposed to currency. What this means for U.S. consumers is that property such as stocks, real-estate and gold is now treated the same as cryptocurrency. When selling stocks, you are expected to report your capital gains and losses, and now the same applies to cryptocurrency. Cryptocurrency tax avoidance goes in breach of IRS regulations. Transactions undergo capital gains tax and that must be reported on Form 8949, the same applies to cryptocurrencies.

Regarding enforcement, cryptocurrency is treated just like any other asset by the IRS. Any trader or investor is expected to accurately report any taxes owed and pay all due taxes by the annual deadline.

Failure to do this can lead to significant sanctions, including fines and penalties. For more serious cases, the IRS may pursue tax evasion charges, meaning that jail is also a possibility.

In order to ensure this never happens, it’s incumbent upon traders to keep accurate records. This means detailing every trade or transaction made. This includes all trades on exchanges, all third-party sales, and trades and all transactions.

If you’re a day trader, that can mean compiling data for thousands of separate trades. Fortunately, most exchanges allow traders to print out a record of all trades. Additionally, advanced portfolio tracking tools can help you track trades from multiple sources with ease. This information is critically important, as it can help you (or a third-party tax professional) accurately calculate your year-end taxes.

Working with a tax professional is often a smart move for most traders and investors, as the high volatility of the digital currency market makes it difficult to track profits and losses with precision. Additionally, working with a professional can help ensure that you receive the tax advantages to which you’re entitled while avoiding the kind of mistakes that can lead you to tax trouble.

The Takeaway

Taxes on cryptocurrency trading and transactions can be a difficult subject for even experienced traders and investors. By understanding the information we’ve outlined above, you can help ensure that you stay on the right side of the law.

Our sophisticated crypto trading bot uses advanced technology to help keep your trades, gains, and losses in order so you’ll be more prepared when tax time comes.